I often receive calls and emails from clients that go something like this:

“Hi Marcus, I’m thinking of purchasing a new car (or a delivery vehicle for the business), what’s the best way to make it the most tax effective?”

“What entity should I purchase it in?”

“Should I purchase it outright, finance the vehicle or lease it?”

At some point, many of us have thought this, because purchasing a vehicle can be a costly exercise, and structuring it poorly can have negative tax consequences. Also, the reality is we spend a lot of money running our vehicles, and many business owners and even employees use their vehicles for genuine work purposes, so what does the ATO say about claiming motor vehicle expenses.

There are two methods available to claim motor vehicle expenses for cars. These exclude ‘other vehicles’, which are defined as motorcycles, utility trucks and panel vans and are applicable to individuals, including business owners and employees who own or lease the car.

1. Cents per kilometre method

· Fixed rate for each kilometre travelled for business. For the 2025 financial year, the rate is $0.88 per km.

· Claim up to a maximum of 5,000 business kilometres per car, per year.

· No written evidence required but need to be able to explain basis for km claim.

· Covers all expenses (fuel, servicing, depreciation, insurance, rego).

2. Logbook method

· Must keep a valid logbook for a minimum continuous 12-week period (valid for 5 years unless circumstances change).

· Record kilometres travelled, reason and date for each journey for the 12-week period.

· Note the car’s odometer readings at the start and end of the logbook period (total kms).

· Calculate the business use percentage for the logbook period.

· Written evidence of expenses required for actual costs, such as fuel, servicing, repairs, rego, insurance, depreciation, lease payments and interest.

· The business use percentage is then applied to the total actual running costs to determine the tax deduction.

So which method is the best for you?

The cents per kilometre method is much simpler and requires far less record-keeping. There also is no need to provide your accountant details of all your actual motor vehicle expenses for the financial year. However, it is capped at 5,000kms ($4,400 for the 2025 financial year). Generally, this method is best suited for those who have a relatively low business use, and their running expenses are relatively cheap.

The logbook method can provide a greater tax deduction for those with a high business use, because the business portion of all actual costs can be claimed, including larger costs like loan interest and depreciation. With that said, there are far more record keeping requirements, is scrutinised more by the ATO and may not be worth the effort when you have a low amount of business travel.

Business Vehicles

Many pharmacies have a dedicated vehicle for delivery services. If there is clear evidence of no private use, no logbook is required, and the running costs are 100% deductible in the business. To ensure there is no evidence of private use, the car should be kept at the business premises and have a policy in place restricting private use.

If the car is used also for personal reasons, a logbook will need to be maintained to ensure the personal travel is excluded from the deduction.

These cars would be treated like many other business assets, purchased in the business entity, and accounted for in the business accounts. The car does not necessarily need to be brand new. Small businesses with an aggregated turnover less than $10 million, can use the simplified depreciation rules. This means a delivery vehicle less than $20,000 can be fully expensed in the year of purchase (if you can find a car that cheap!).

Other Considerations

Depreciation: The ATO has a car limit. If your car is more than $69,674, the excess cannot be claimed for tax depreciation. Remember, depreciation does not apply if you opt to use the cents per kilometre method as that fixed rate covers all expenses.

Goods and Services Tax (GST):

If you’re registered for GST, obtain a tax invoice and the vehicle is solely or partly used in carrying on your businesses, you can claim a GST credit on the business portion. For example, if the business use is 40%, you can claim that portion.

Generally, if you purchase a car and the price is more than the car limit mentioned earlier, the maximum amount of GST credit you can claim is one-eleventh of that limit.

Fringe Benefits Tax (FBT): A car fringe benefit commonly arises where you make a car you own or lease available for an employee’s private use. In most cases, the business will be liable for FBT, unless the type of vehicle meets the criteria to be exempt for FBT. Some exempt vehicles include:

· Single cab utes

· Dual cab utes with a 1 tonne carry load or more

· Battery electric vehicle or hydrogen fuel cell electric vehicles if luxury car tax (LCT) was never payable on the importation or sale of the car.

Even if you purchase a second-hand EV, if LCT was payable on that car previously, the car will no longer be exempt for FBT purposes.

FBT can be complex, so it’s important you consult with your accountant to understand your specific circumstances, so you don’t get caught out.

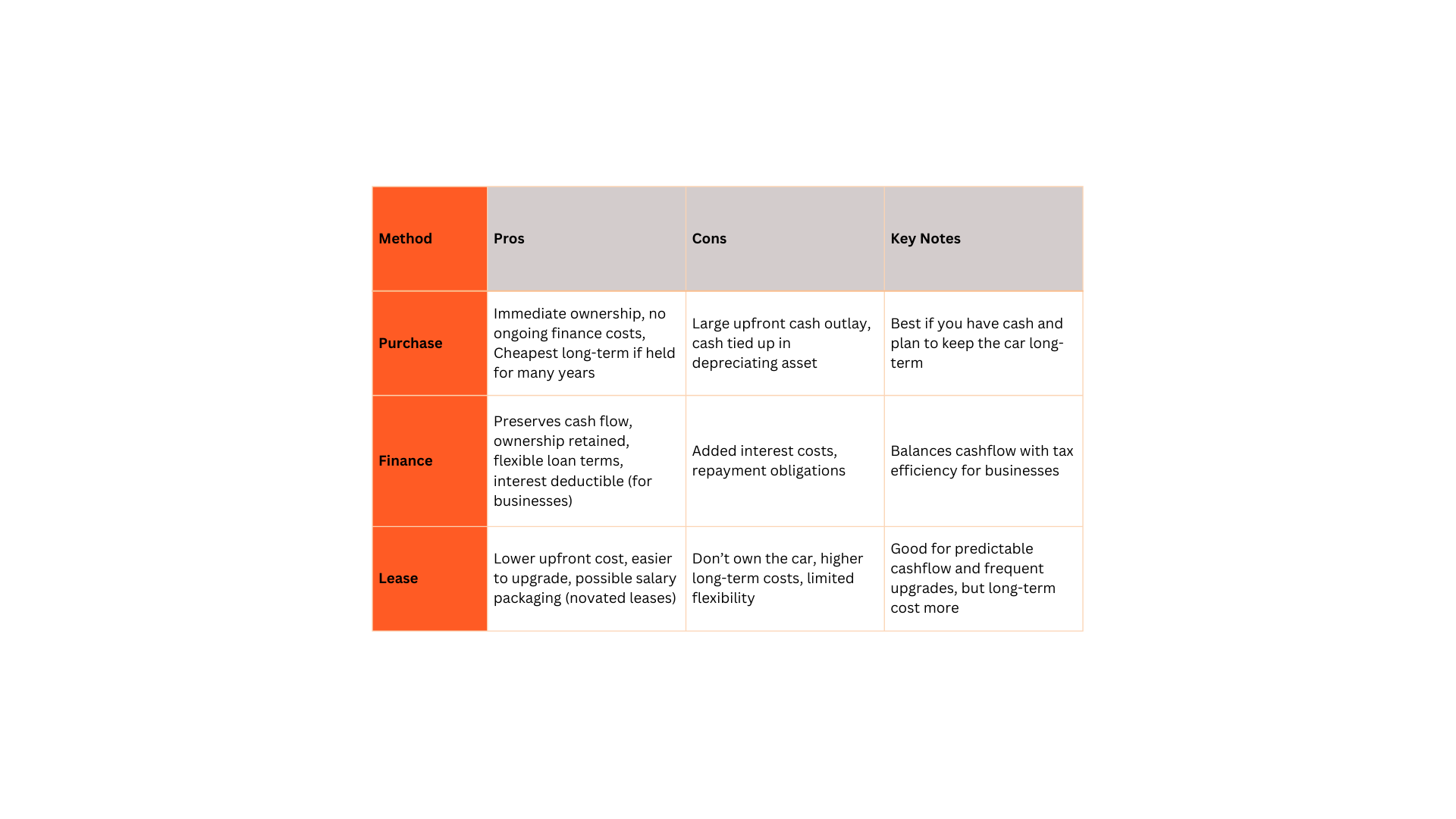

Should I Purchase, Finance, or Lease a Vehicle?

Below are some practical considerations.

Conclusion

When the time comes for you to purchase a vehicle and organise your motor vehicle claims for tax time, consider how often you are using your vehicle for work-related purposes and which method you think is best. Watch out for FBT (even for owners), and always keep good records to protect you in case of an ATO review.

If you’re unsure which method or ownership option is best for your circumstances, consult with your accountant. A little planning up front can save you both time and money down the road—and give you the confidence that your vehicle decisions are fully tax-smart.